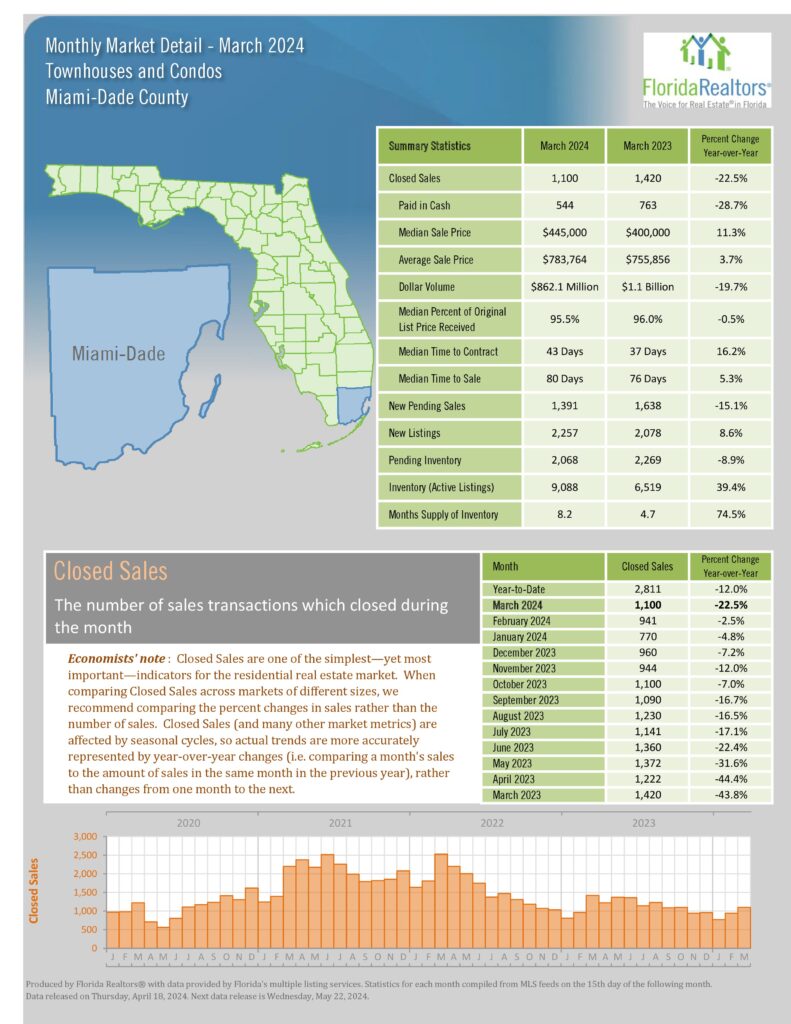

Miami Real Estate Report, March 2024 Statistics

KEY NUMBERS (Compared to March 2023)

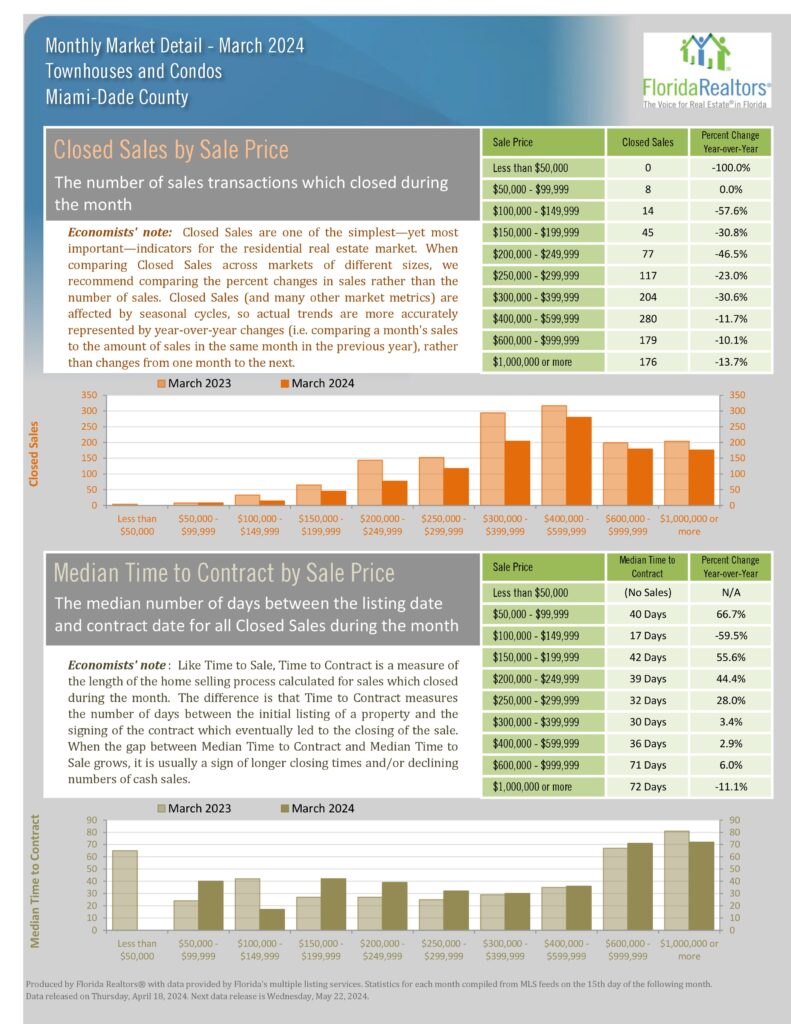

· Number of Condo Sales Down 22.5%

· Number of SFH Sales Down 4.8%

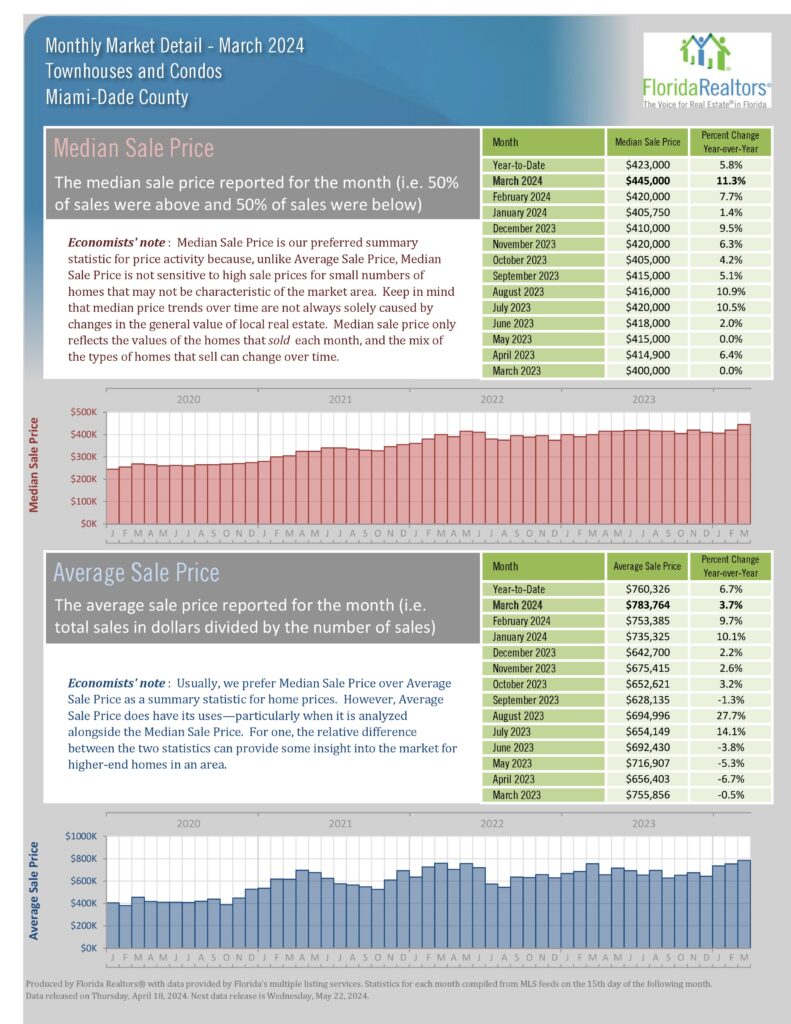

· Median Condo Price –

Up 11.3%

· Median SFH Price Up 14%

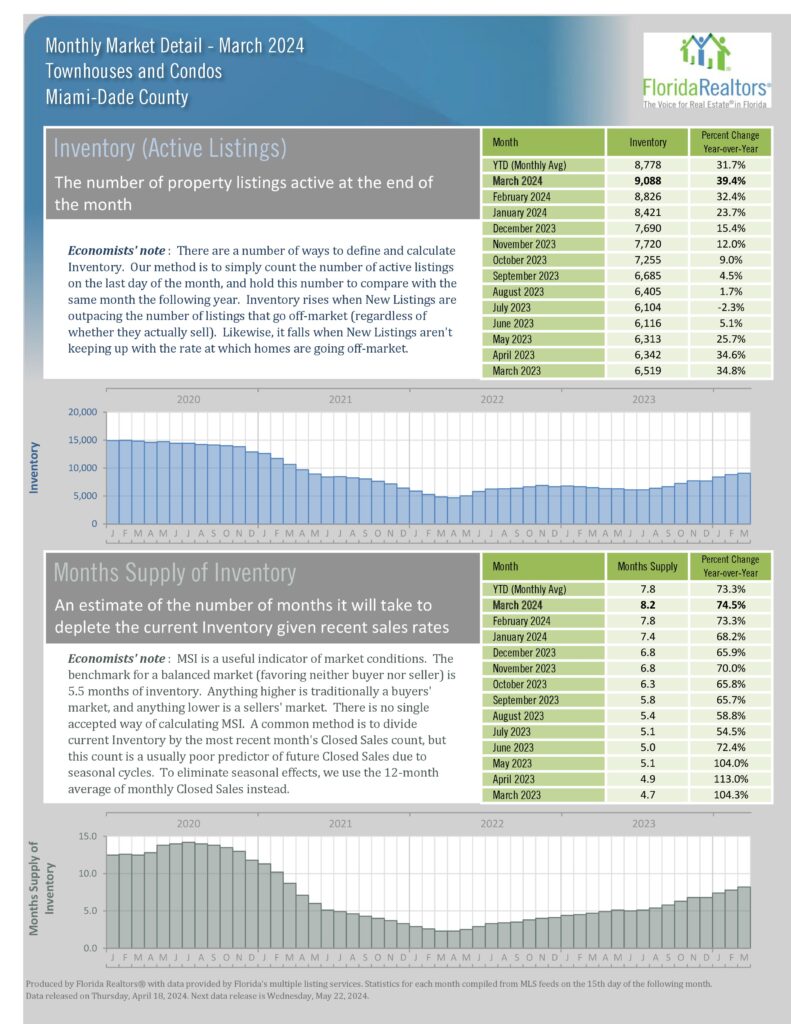

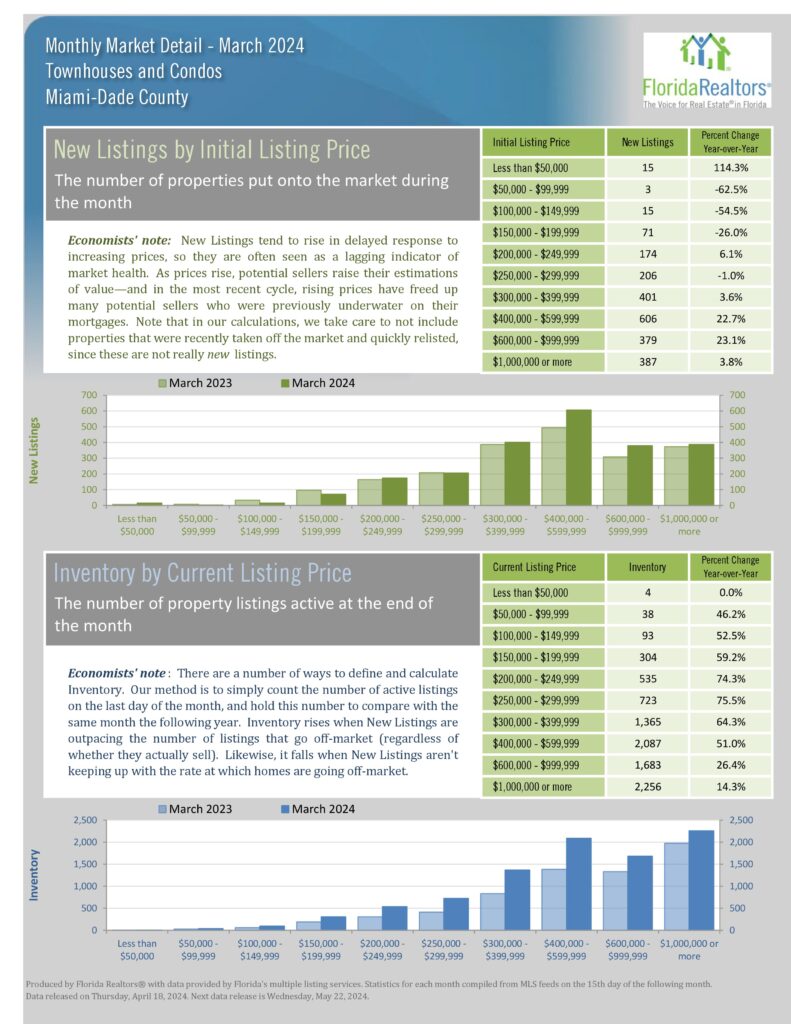

· Inventory

Condos Up 39.4%

SFH Up 14.2%

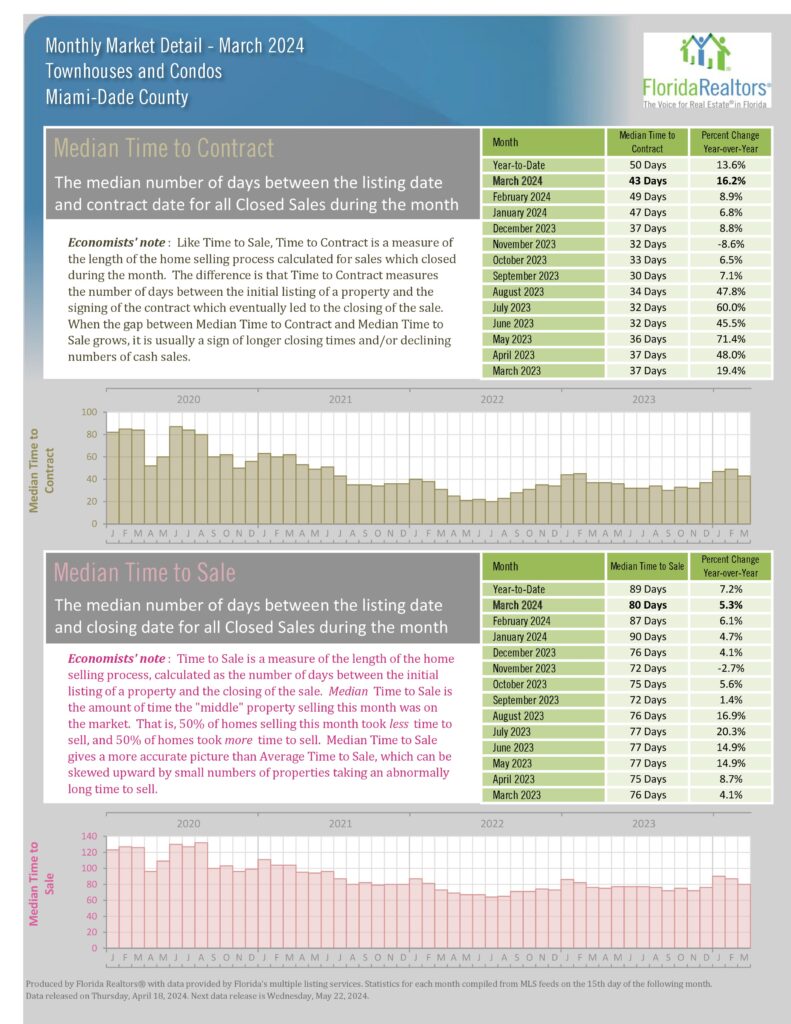

· Days On Market

Condos 43 Days

SFH 31 Days

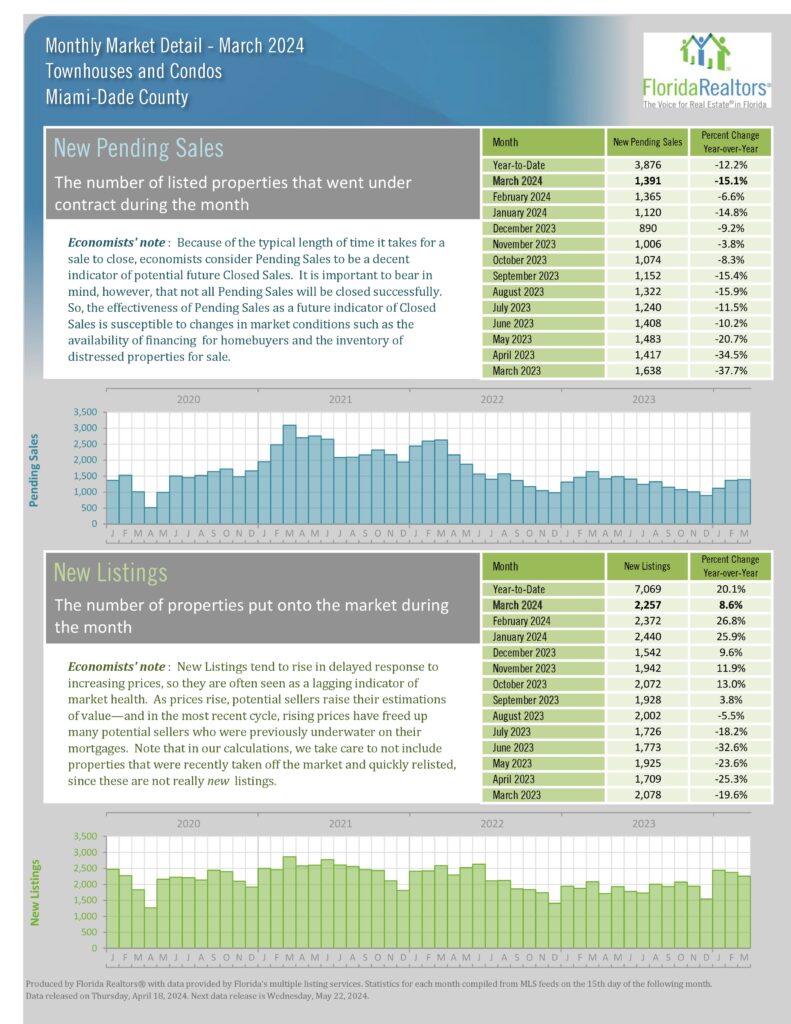

· Pending Inventory

Condos Down 8.9%

SFH Down 4%

Months Supply

· Condos 8.2 months

· SFH 4.3 months

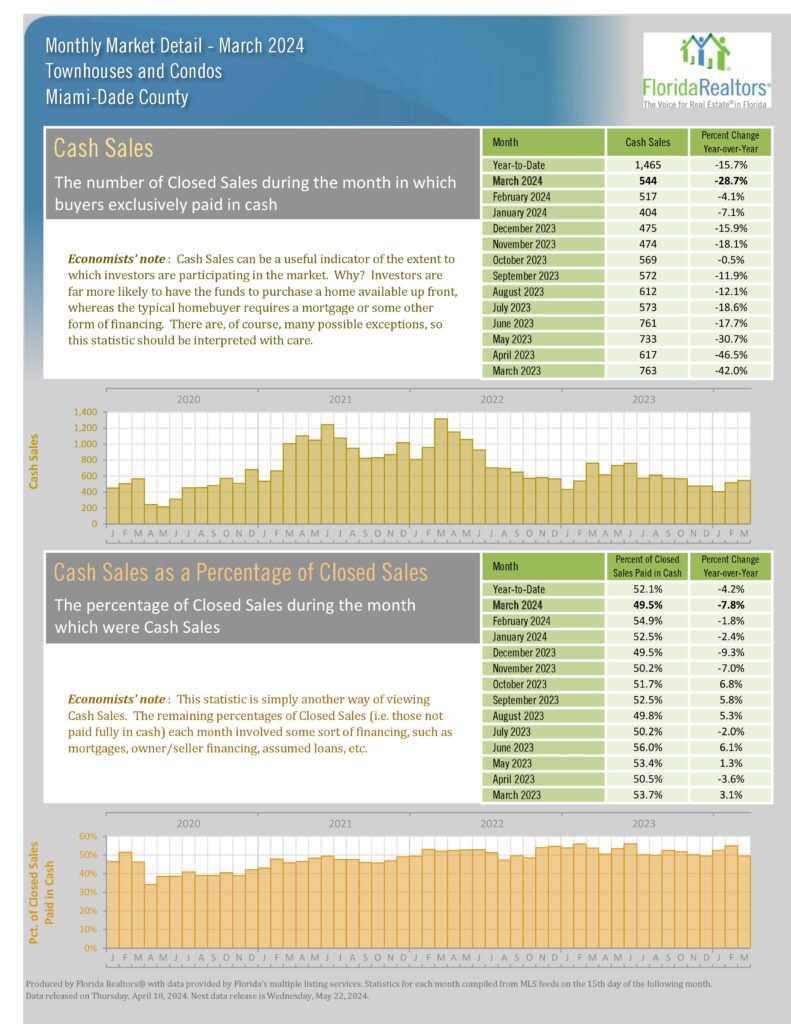

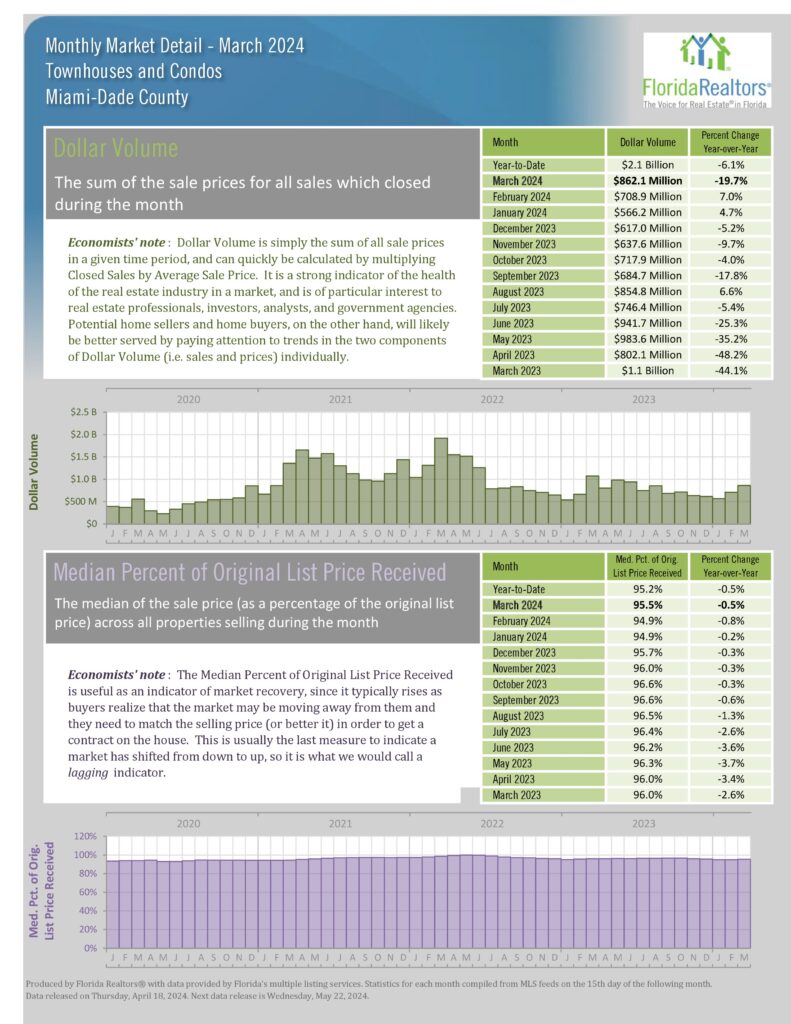

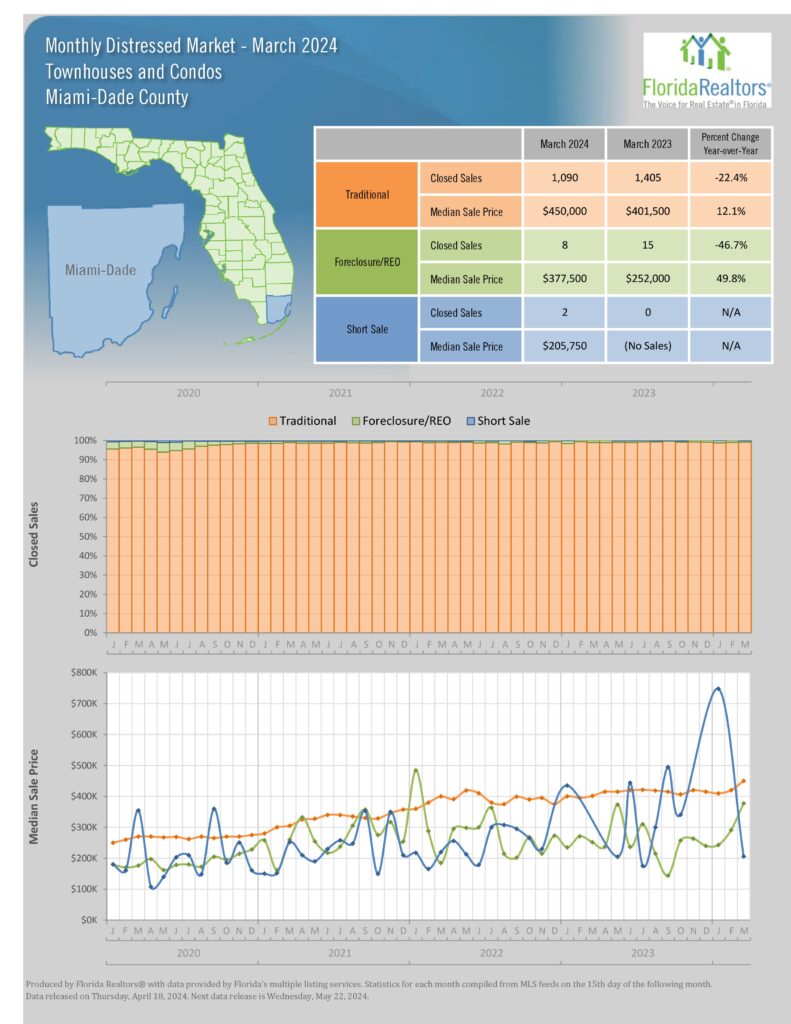

Closed Condo sales in March were down 22.5% from March 2023 and 10% down from March 2020 – pre-pandemic – when interest rates were low. The Miami Condo market has a high rate of cash sales accounting for 49.5% in March but because of high interest rates, demand is still sluggish. Many buyers needing financing are still on the sidelines. Inventory is good with a 8.2 month supply (a balanced market is recognized as having a 6-to-9-month supply of inventory) but the high interest rates are keeping the demand slowed down.

Single family home closed sales were down 4.8%, but the number of monthly sales was the highest since last April. Sales in the $1million plus range were up 22.9% and the $600k-$1mil. range up 19.9%. New pending sales for both condos and single family saw a drop starting in 3Q23, but both are experiencing increases in the first 3 months of this year. Median Condo price at $445k was up 11.3% compared to last March while Single family Median Price was up 14%, and all time high. with a 4.4-month supply -still in Seller’s market territory. Year to date, 27.4% of SFH sales were cash – much higher than the national average. Distressed sales represented just 0.8% of all sales. This is not a distressed market. Solid values, strong cash sales, increased inventory are all good indicators, but lower interest rates would increase sales.